This post was originally published on this site

What Is the Cost of Debt?

The cost of debt is the total interest expense owed on a debt. Put simply, the cost of debt is the effective interest rate or the total amount of interest that a company or individual owes on any liabilities, such as bonds and loans. This expense can refer to either the before-tax or after-tax cost of debt. The degree of the cost of debt depends entirely on the borrower’s creditworthiness, so higher costs mean the borrower is considered risky.

KEY TAKEAWAYS

- The cost of debt is the effective rate that a company pays on its debt, such as bonds and loans.

- The key difference between the pretax cost of debt and the after-tax cost of debt is the fact that interest expense is tax-deductible.

- Debt is one part of a company’s capital structure, with the other being equity.

- Calculating the cost of debt involves finding the average interest paid on all of a company’s debts.

Investopedia / Julie Bang

How the Cost of Debt Works

Debt is any money owed by one entity to another. Having debt is unavoidable for many entities and is rather common. In fact, companies and individuals may use debt to make large purchases or investments for further growth.

For corporations. debt is one part of their capital structures, which also includes equity. Capital structure deals with how a firm finances its overall operations and growth through different sources of funds, which may include debt such as bonds or loans.

The cost of debt measure is helpful in understanding the overall rate being paid by a company to use these types of debt financing. The measure can also give investors an idea of the company’s risk level compared to others because riskier companies generally have a higher cost of debt.

The cost of debt is generally lower than cost of equity.

Formula and Calculation of Cost of Debt

There are a couple of different ways to calculate a company’s cost of debt, depending on the information available.

After-Tax Cost of Debt

One way to calculate the cost of debt is by using the formula for the after-tax cost of debt:

The risk-free rate of return is the theoretical rate of return of an investment with zero risk, most commonly associated with U.S. Treasury bonds. A credit spread is a difference in yield between a U.S. Treasury bond and another debt security of the same maturity but different credit quality.

This formula is useful because it takes into account fluctuations in the economy, as well as company-specific debt usage and credit rating. If the company has more debt or a low credit rating, then its credit spread will be higher.

For example, say the risk-free rate of return is 1.5% and the company’s credit spread is 3%. Its pretax cost of debt is 4.5%. If its tax rate is 30%, then the after-tax cost of debt is 3.15%. We can calculate this in the following way:

[(0.015+0.03)×(1−0.3)][(0.015+0.03)×(1−0.3)]

Before-Tax Cost of Debt

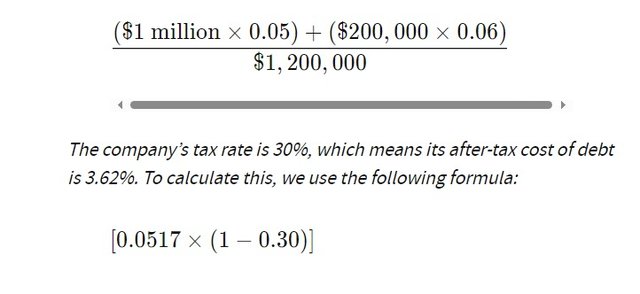

Another way to calculate the cost of debt is to determine the total amount of interest paid on each debt for the year. The interest rate that a company pays on its debts includes both the risk-free rate of return and the credit spread from the formula above because the lender(s) will take both into account when initially determining an interest rate.

Once the company has its total interest paid for the year, it divides this number by the total of all of its debt. This is the company’s average interest rate on all of its debt.

For example, say a company has a $1 million loan with a 5% interest rate and a $200,000 loan with a 6% rate. The average interest rate and its pretax cost of debt is 5.17%. This is calculated as follows:

Fast Fact: The cost of debt before taking taxes into account is called the before-tax cost of debt. The after-tax cost of debt already factors in taxation. The key difference in the cost of debt before and after taxes lies in the fact that interest expenses are tax-deductible.

Impact of Taxes on Cost of Debt

Since the interest paid on debts is often treated favorably by tax codes, the tax deductions due to outstanding debts can lower the effective cost of debt paid by a borrower.

The after-tax cost of debt is the interest paid on debt less any income tax savings due to deductible interest expenses. To calculate the after-tax cost of debt, subtract a company’s effective tax rate from one, and multiply the difference by its cost of debt. The company’s marginal tax rate is not used. Instead, the company’s state and federal tax rates are added together to ascertain its effective tax rate.

For example, if a company’s only debt is a bond that it issued with a 5% rate, then its pretax cost of debt is 5%. If its effective tax rate is 30%, then the difference between 100% and 30% is 70%, and 70% of the 5% is 3.5%. The after-tax cost of debt is 3.5%. The rationale behind this calculation is based on the tax savings that the company receives from claiming its interest as a business expense.

Using the example, imagine the company issued $100,000 in bonds at a 5% rate with annual interest payments of $5,000. It claims this amount as an expense, which lowers the company’s income by $5,000. As the company pays a 30% tax rate, it saves $1,500 in taxes by writing off its interest. As a result, the company effectively only pays $3,500 on its debt. This equates to a 3.5% interest rate on its debt.

How to Reduce Cost of Debt

Cutting expenses down is a key goal for corporations and individuals. Whether it’s an individual or corporation, the goal is usually the same: to keep costs down and revenue/income higher. Having said that, there are ways to reduce the cost of debt. The following are just a few of the ways to do so:

- Negotiating Rates: Consider the situation and see if you can negotiate a better rate. Some lenders will offer a certain rate upfront. But you don’t have to accept the rate they give you. In fact, many lenders may be willing to work with you to give you a lower one if you are willing to put in the effort to negotiate because they want your business.

- Refinancing: Consider refinancing if interest rates lower or your situation changes and you’re in a position to secure a better rate. People often do this with their mortgages when interest rates drop. This allows them to cut their monthly mortgage payments down.

- Increase Payments: If you pay more than the required monthly payment, you’ll drop your principal balance down, which can reduce the amount of interest you’ll pay over the life of the debt.

- Improving Credit Scores: Your credit score is what determines the rate you’re going to get. If you have a low score, you’ll end up paying a higher rate. Improving your score will help you get a lower rate. You can do this by maintaining your payments or paying off existing debt. Make sure you check your credit report regularly to ensure there are no errors.

Example of Cost of Debt

We’ve shown a few instances of the cost of debt. But let’s take a look at one final example to show how it works.

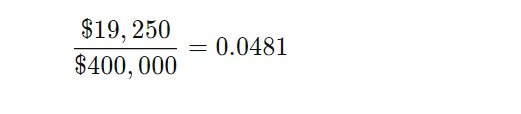

Suppose you run a small business and you have two debt vehicles under the enterprise. The first is a loan worth $250,000 through a major financial institution. The second is a $150,000 loan through a private investor. The first loan has an interest rate of 5% and the second one has a rate of 4.5%.

First, let’s calculate the total amount of interest you’ll pay each year on both of these loans:

- Loan # 1: $250,000 x 5% = $12,500

- Loan # 2: $150,000 x 4.5% = $6,750

We can add these two figures together to get the total annual interest, which is $19250.

In order to calculate the effective rate before taxes, we divide this figure by the total amount of the debt:

Therefore, the effective before-tax rate of these debts is 4.81%

Why Does Debt Have a Cost?

Lenders require that borrowers pay back the principal amount of debt, as well as interest in addition to that amount. The interest rate, or yield, demanded by creditors is the cost of debt—it is demanded to account for the time value of money (TVM), inflation, and the risk that the loan will not be repaid. It also involves the opportunity costs associated with the money used for the loan not being put to use elsewhere.

What Makes the Cost of Debt Increase?

Several factors can increase the cost of debt, depending on the level of risk to the lender. These include a longer payback period, since the longer a loan is outstanding, the greater the effects of the time value of money and opportunity costs. The riskier the borrower is, the greater the cost of debt since there is a higher chance that the debt will default and the lender will not be repaid in full or in part. Backing a loan with collateral lowers the cost of debt, while unsecured debts will have higher costs.

How Do Cost of Debt and Cost of Equity Differ?

Debt and equity capital both provide businesses with the money they need to maintain their day-to-day operations. Equity capital tends to be more expensive for companies and does not have a favorable tax treatment. Too much debt financing, however, can lead to creditworthiness issues and increase the risk of default or bankruptcy. As a result, firms look to optimize their weighted average cost of capital (WACC) across debt and equity.

What Is the Agency Cost of Debt?

The agency cost of debt is the conflict that arises between shareholders and debtholders of a public company when debtholders place limits on the use of the firm’s capital if they believe that management will take actions that favor equity shareholders instead of debtholders. As a result, debtholders will place covenants on the use of capital, such as adherence to certain financial metrics, which, if broken, allows the debtholders to call back their capital.

The Bottom Line

Debt is unavoidable for most people and businesses. It can help us make major purchases or help finance our growth. But it’s important to understand how it works. Not only are you paying the principal balance, but you’re also responsible for the interest. This is referred to as the cost of debt. You can figure out what the cost of debt is by multiplying the value of your loan by the annual interest rate. Determine your effective interest rate by adding together all that interest by the total amount of debt you owe.